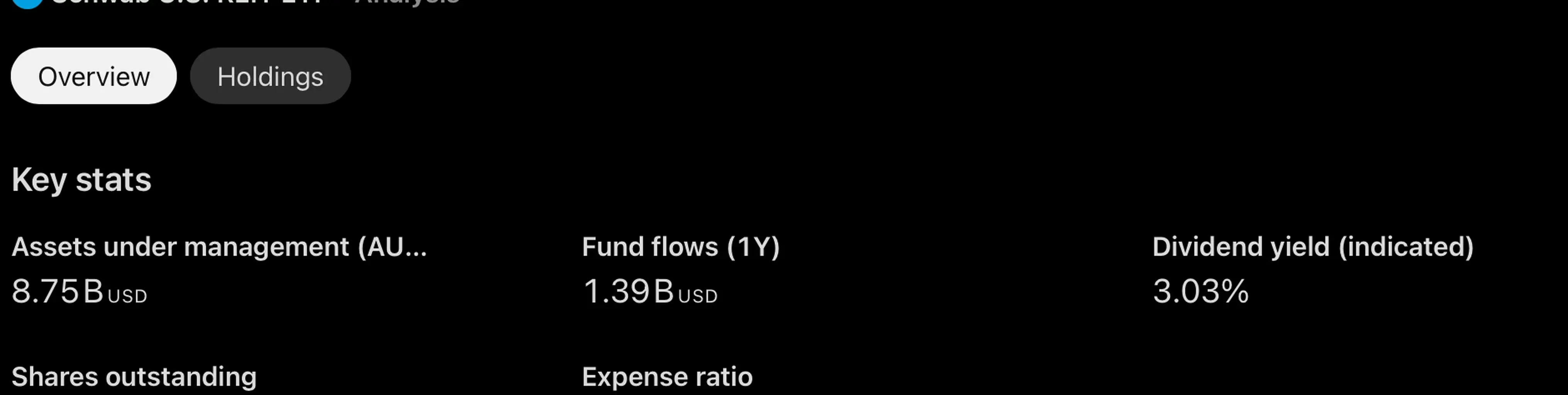

No price targets are provided for SCHH. It is presented as a steady dividend income holding. Current price is 21.00. The fund tracks an index of roughly 120 publicly traded equity REITs and is rebalanced quarterly to maintain diversification while keeping costs low. As an income-generating asset total return tends to be driven more by dividends than by price appreciation.

- Apartments & residential

- Industrial warehouses

- Retail & shopping centers

- Data centers

- Healthcare & storage

- Office

A shifting macro backdrop is becoming more supportive for REITs. Lower interest rates reduce financing costs which can stabilize or lift property values and make dividend yields more attractive versus bonds. Improved cash flows enable refinancing acquisitions and potential dividend support. Structural demand drivers cited include logistics and warehouses tied to e-commerce data centers driven by AI and cloud growth and residential markets affected by housing shortages. REITs are positioned to serve both income and diversification roles heading into 2026 and beyond.

Edwards LifeSciences is trading near yearly highs following FDA approval of the SAPIEN M3 system. The SAPIEN M3 is a minimally invasive mitral valve replacement option for patients with moderate to severe mitral valve leakage who are not candidates for open-heart surgery or existing catheter-based repair alternatives. The approval expands Edwards' transcatheter portfolio and adds a less invasive treatment intended to reduce valve leakage and improve symptoms and outcomes for eligible patients.

Edwards is a leader in structural heart disease and therapies that offer alternatives to open-heart surgery. The company has generated billions from heart valve and transcatheter products. Recent reported results show revenue growth of 12% and 14.7% in the last two quarters and a 72% surge in free cash flow. Acquisitions such as Endotronix and the planned JenaValve transaction - if approved - broaden the company’s reach into heart failure monitoring and more complex valve conditions. The stock is trading near annual highs so some positive developments may already be reflected in the price.

Global defense spending trends cited include compound annual growth rates ranging from 4.9% to over 8% for the mid 2020s with total spending last year estimated near $2.7 trillion and projections toward $6 trillion by 2035. Lockheed Martin is described as the world’s largest defense contractor supplying combat aircraft such as the F-35 missiles and precision strike weapons helicopters including the Black Hawk radar systems and space systems and satellites.

The company reports a backlog of more than $176 billion. Contract awards noted include the largest Patriot missile contract in history awarded by the U.S. Army and a $10.85B contract from the U.S. Marine Corps. Financially the stock has been relatively flat over the past three years with revenue prior to this year showing limited growth while peers RTX and NOC expanded sales. Recent updates show revenue recovery this year with the last quarter up 8.8% and guidance and outlook increases for both revenue and earnings reported.

This material is provided for informational and educational purposes only and does not constitute financial advice. All investments carry risk, including the potential loss of capital.

Feed